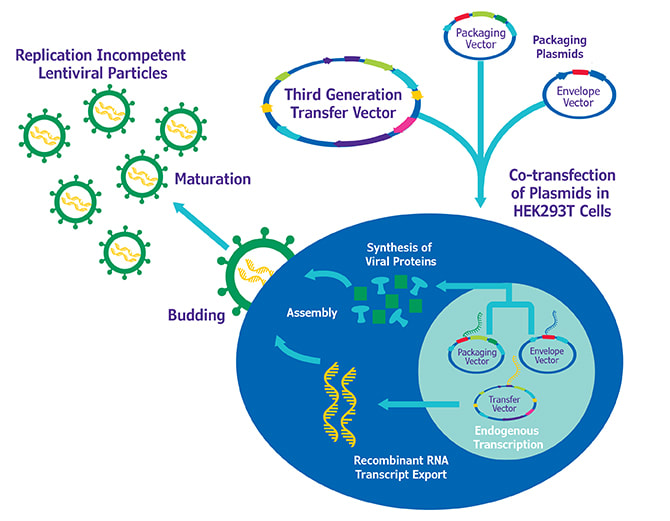

Lentiviral Vectors Market They are derived from HIV and have the ability to efficiently deliver therapeutic and research genes into both proliferating and non-proliferating cells. Lentiviral vectors offer several advantages over other types of gene delivery systems including high transduction efficiency, stable transgene expression, and the ability to transduce non-dividing cells. They have emerged as a promising alternative to gammaretroviral and adenoviral vectors for applications in gene therapy, cell engineering, and other life science research areas.

The global lentiviral vectors market is estimated to be valued at US$ 336.39 Bn in 2024 and is expected to exhibit a CAGR of 13% over the forecast period 2024 to 2031. Key Takeaways Key players: Key players operating in the lentiviral vectors market include Tata Communications Ltd., Amazon CloudFront– Amazon.com Inc., Cachefly, CDNetworks Co., Ltd., CDNify Ltd., CDNsun, CDNvideo, CloudFlare, Inc., EdgeCast Networks, Fastly, Proinity LLC, Limelight Networks Inc., Skypark CDN, and Level 3 Communication Inc. Major players are focused on expanding their product portfolios and global footprint via partnerships and acquisitions. Growing demand: Lentiviral Vectors Market Increasing prevalence of genetic disorders, cancer, and infectious diseases along with rising funding for gene therapy research is expected to drive the demand for lentiviral vectors over the forecast period. They offer promising treatment alternatives and are being extensively researched for development of new gene therapies. Global expansion: Leading companies are focused on expanding their manufacturing facilities and establishing production units in different geographies to cater to the growing global demand. For instance, in 2020, Pharming Group N.V. set up a new facility in the US to enhance manufacturing of lentiviral vectors. Several firms are also investing in developing lentiviral vector platforms optimized for various therapy areas. Market key trends CRISPR technology integration: Lentiviral vector platforms are being combined with CRISPR/Cas9 genome editing tools to develop more targeted and efficient gene therapies. This trend allows delivery of CRISPR components like Cas9 and sgRNAs using vectors for in vivo therapeutic applications. Focus on scalable production: Major players are investing in automated, scalable manufacturing techniques to increase lentiviral vector yields and support large-scale clinical trials and commercialization. This is important for enhancing process consistency and reducing costs. Porter's Analysis Threat of new entrants: The biotechnology and pharmaceutical industry requires high capital investments limiting threat of new entrants. However, the lentiviral vectors market has relatively lower entry barriers. Bargaining power of buyers: Due to several key players in the market, buyers have high bargaining power to negotiate on pricing. However, requirement of technical expertise limits bargaining power. Bargaining power of suppliers: Suppliers of raw materials have moderate bargaining power due to availability of substitute materials suppliers. Threat of new substitutes: New cell and gene therapy modalities pose threat of substitution. However, lentiviral vectors are established with no direct substitute. Competitive rivalry: The market is dominated by few players intensifying competition. Players differentiate through product portfolio expansion. Geographical Regions North America region dominated the global lentiviral vectors market in terms of value in 2024 due to extensive research in gene and cell therapy along with presence of major market players. The United States contributed significantly to North America due to well-established biopharmaceutical industry and healthcare infrastructure supporting clinical research. The Asia Pacific region is expected to witness the fastest growth during the forecast period from 2024 to 2031. This is attributed to factors such as increasing healthcare investments, expanding biopharmaceutical industry, and growing research funding for developing novel gene and cell therapies in countries including China and India. Rising disease burden and growing awareness create demand for advanced treatment such as lentiviral vectors based gene therapy in Asia Pacific.

0 Comments

Corn Gluten Feed Market The global corn gluten feed market is witnessing a steady growth due to its increased adoption in animal feed supplements as a protein-rich alternative to soybean and fish meals. Corn gluten feed is a co-product of the corn-wet milling process that produces corn syrup, high fructose corn syrup, and dextrose. It is made from leftovers of corn after removing starch. Corn gluten feed is considered an economical source of protein in animal feed rations. It contains 20-30% of crude protein that includes multiple amino acids making it a viable replacement for soybean and fish meals.

The Global corn gluten feed market is estimated to be valued at US$ 8.45 Bn in 2024 and is expected to exhibit a CAGR of 12% over the forecast period 2024 to 2031. Key Takeaways Key players operating in the corn gluten feed market are Adidas, Suunto, Abbott laboratories, Sony, Eurotech, Nike, Google, Inc., Garmin International Inc., Medtronic, Fitbit Inc., and Apple Inc. The key opportunities in the global corn gluten feed market include its rising usage as a sustainable and affordable alternative to conventional protein sources as well as focus on expanding production capacities. Manufacturers are focusing on increasing the production of corn gluten feed through capacity expansion projects, especially in Asia Pacific and North America where the demand is rising rapidly. The growing animal feed industry across the globe coupled with shift towards natural feed ingredients over antibiotics is supporting the growth of the corn gluten feed market. Countries like China, the U.S., Brazil, and India offer lucrative growth opportunities owing to large livestock populations and rising meat consumption in these regions. Market Drivers The major market driver for increasing demand of corn gluten feed is its economical cost as compared to conventional protein sources like soybean and fish meals. Corn gluten feed Market Size provides comparable nutritional value at lower prices. As the production of biofuel ethanol from corn starch increases globally, the supply of corn gluten feed as a co-product also rises, keeping its prices low. This makes it an attractive proposition for animal feed producers to use corn gluten feed without significantly increasing their input costs. PEST Analysis Political: Corn gluten is fed to livestock, so any changes in agricultural policies or subsidies could impact demand. Farm bills and trade policies also influence commodity prices and exports. Economic: A strong economy increases demand for meat and dairy, boosting demand for corn gluten feed. High commodity prices make it a cost-effective alternative tocorn. Inflation and energy costs affect feed production. Social: Consumer interest in sustainably and ethically produced food influences farmer practices and demand for local/organic feed ingredients like corn gluten. Population growth and increasing incomes in developing nations drive demand for animal proteins. Technological: Advances in feed formulations and compounding improve the nutritional value and digestibility of corn gluten feed. Traceability technologies help ensure quality and safety. Sustainable farming techniques increase corn gluten yields. Geographical concentration: The market is concentrated in North America and Western Europe due to large-scale meat and dairy production. The U.S. is the top producer and consumer of corn gluten feed worldwide due to intensive cattle, hog and poultry farming. Fastest growing region: Asia Pacific is growing rapidly due to rising incomes, urbanization and westernization of diets in countries like China and India. The region is investing in largescale concentrated animal farming to meet burgeoning demand for meat and dairy. This is driving increased imports and local production of high-quality feed ingredients including corn gluten.  Spark Plugs Market The spark plugs market is an essential component of automotive engine systems. Spark plugs help in igniting the air-fuel mixture within cylinders, allowing for combustion and power generation. Modern spark plugs feature platinum or iridium alloy materials that offer high melting points and resist corrosion, enabling enhanced ignition consistency even in adverse conditions. The global spark plugs demand originates primarily from the automotive industry as all combustion engines require spark plugs for functioning. The rising vehicle production and expanding automotive parc are fueling consumptions.

The Global Spark Plugs Market is estimated to be valued at US$ 3.52 Bn in 2024 and is expected to exhibit a CAGR of 4.8% over the forecast period 2024 to 2031. Key Takeaways Key Players Key players operating in the Spark Plugs Market Size are focusing on introducing new product varieties featuring advanced materials and enhanced Functionalities. For instance, DENSO Corporation offers iridium alloy spark plugs that provide exceptional ignition performance even under extreme conditions. Growing Demand The demand for spark plugs is increasing owing to the rising vehicle parc globally along with stringent emissions regulations mandating frequent spark plug replacement. The proliferation of gasoline engines further supports market growth. Global Expansion Major spark plug manufacturers are expanding their global footprint through new facilities, especially in developing Asian and Latin American markets. For instance, in 2023, NGK Spark Plug Co., Ltd plans to set up a new manufacturing plant in Mexico to cater to the North American free trade agreement region. Market Key Trends One of the key trends gaining traction in the spark plugs market is the rising popularity of advanced spark plug technologies that offer superior performance. Double platinum spark plugs featuring two separate ground and center electrodes coated with platinum provide enhanced ignitability. These double platinum spark plugs are seeing higher demand in performance-oriented vehicles. Porter’s Analysis Threat of new entrants: Existing automotive companies have strong brands and capital which makes it difficult for newcomers to enter. Bargaining power of buyers: Automobile manufacturers are large corporations with significant bargaining power over spark plug producers due to their demand. Bargaining power of suppliers: Key raw materials like metals are commodity products available from numerous suppliers at competitive prices limiting supplier power. Threat of new substitutes: No close substitutes exist for spark plugs as they are integral to internal combustion engines. Competitive rivalry: Competition is intense between major players like DENSO, Bosch, and NGK trying to increase market share through innovations. Geographical Regions North America holds the largest share in terms of value owing to established automotive industry and presence of leading players. The region accounted for over 30% market share in 2024. Asia Pacific excluding Japan is the fastest growing region expected to witness a CAGR of around 6% during the forecast period. Increasing vehicle production and sales in countries like China and India is driving demand for spark plugs.  Bacterial Colony Counters Market The bacterial colony counters market provides significant advantages in microbiological testing for quality control. Automated bacterial colony counters save time and ensure accurate and reliable microbial enumeration compared to manual colony counting. Precise determination of microbial load is critical in pharmaceutical and food testing applications to validate product safety and shelf life. The growing need for reproducible and error-free colony counting in various industry verticals is propelling the adoption of bacterial colony counters.

The global bacterial colony counters market is estimated to be valued at US$ 592.7 Mn in 2024 and is expected to exhibit a CAGR of 4.2% over the forecast period 2024 to 2031. Key Takeaways Key players: Key players operating in the bacterial colony counters market are Environmental & Scientific Instruments Co., Interscience, Neu-tec Group Inc., Thermo Fisher Scientific Inc., AVI Scientific India, Isolab Laborgeräte GmbH, Scitek Global Co., Ltd., Infitek Co., Ltd., ESICO INTERNATIONAL, Biolab Scientific, Cole-Parmer Instrument Company, LLC., Analytik Jena GmbH+Co. KG, Oxford Optronix, BIOBASE GROUP, Reichert, Inc., and Copan Diagnostics Inc. Key opportunities: Bacterial Colony Counters Market Size Rising awareness regarding healthcare-associated infections, growing stringency in pharmaceutical quality control protocols, and favorable government funding for life sciences research present significant growth opportunities. Global expansion: Major players are focusing on expanding their global footprint through strategic acquisitions and partnerships. For instance, Thermo Fisher Scientific acquired Phadia to establish leadership in the clinical diagnostics market and strengthen its international presence. Market drivers: Increasing R&D investments in the healthcare and pharmaceutical industries, rising prevalence of infectious diseases, growing need for sterility testing in the medical device manufacturing sector, and widespread application of bacterial colony counters in food safety testing are major market drivers. Market restraints: High costs associated with automated instruments and dependence on trained professionals for operation are key challenges. However, technological advancements to develop affordable and user-friendly devices will support market growth over the forecast period. Segment Analysis The Bacterial Colony Counters Market can be segmented into manual counters and automatic counters. The automatic counters segment currently dominates the market, accounting for over 60% share. Automatic counters provide various advantages over manual counters such as real-time counting, elimination of human errors, high throughput of samples, and generation of reports. They integrate imaging technologies and software for automatic counting, classification, and analysis of bacterial colonies on agar plates. Their ability to efficiently handle large volumes of samples in clinical, food testing, and other laboratories has resulted in higher preference over manual counters. Global Analysis Regionally, North America holds the largest share in the bacterial colony counters market, and is expected to maintain its dominance during the forecast period. This is attributed to factors such as presence of major players, technological advancements, and rising funding for research activities in the region. The Asia Pacific region is projected to witness the fastest growth during the forecast period driven by expansion of pharmaceutical and biotechnology industries, rising awareness, and growing healthcare expenditure in emerging countries such as China and India. Government initiatives to strengthen healthcare infrastructure are also contributing to market growth in Asia Pacific. Europe holds a substantial share and is expected to exhibit steady growth in demand for bacterial colony counters due to stringent regulations regarding safety and quality of food, water, and pharmaceutical products in the region. Get more insights on This Topic- Bacterial Colony Counters Market  The food grade alcohol market consists of various types of alcohols such as ethanol, isopropanol, and methanol that meet food chemical standards. Ethanol is the major and widely used type of food grade alcohol which is primarily produced from grains such as corn, wheat, barley, or sugars extracted from sugarcane or sugar beets. Food grade alcohol finds extensive applications in beverages such as beer, wine, spirits as well as flavorings, extracts, and food preservatives. Growing health awareness has augmented the demand for low-calorie, low-sugar beverages that utilize alcohol for taste. This, in turn, has boosted the market.

The Global Food Grade Alcohol Market is estimated to be valued at US$ 2.56 Bn in 2024 and is expected to exhibit a CAGR of 5.5% over the forecast period from 2024 to 2031. Key Takeaways Key players operating in the food grade alcohol are MGP, Cargill Incorporated, ADM, Cristalco, Grain Processing Corporation, Wilmar International Ltd., Extractohol, Pure Alcohol Solutions, Nedstar, Sasma B.V., Roquette Frères , Essentica, AVANSCHEM, Fairly Traded Organics, and Ethimex Ltd. Key players focus on strengthening their market presence through strategic acquisitions and new product launches. For instance, in 2021, ADM acquired Tianjin Angel Yeast to expand its yeast portfolio and offerings. The growing demand for alcoholic beverages from the millennial population and increasing preference for high-quality craft beverages are fueling the food grade alcohol market. Moreover, the rising demand for low-calorie beverages made with alcohol is also propelling the market growth. Globally, North America dominates the Food Grade Alcohol Market Size due to increasing consumption of spirits and craft beers. However, Asia Pacific is expected to witness the fastest growth owing to rising disposable incomes, increasing preference for Western drinking culture, and growing urbanization. Furthermore, increasing focus of key players on tapping opportunities in emerging economies is also expected to drive the market in the region. Market Drivers The increasing usage of alcohol in beverages is the major driver augmenting the food grade alcohol market growth. Food grade alcohol acts as a perfect solution for manufacturers seeking to develop low-calorie, low-sugar alcoholic beverages with natural flavors. It allows producing light beers with fewer carbs and low-calorie wines and spirits made without compromising the taste. Thus, the rising demand for healthier alcohol options is propelling the market. The current geopolitical situation is impacting the growth of the food grade alcohol market. Supply chain disruptions due to the Russia-Ukraine conflict and sanctions on Russia have led to increased prices of grains and other key raw materials globally. This is negatively impacting the production volumes and margins of food grade alcohol manufacturers. Moreover, uncertainty around economic growth in Europe and other key markets is dampening demand growth prospects in the short term. Additionally, lingering effects of the COVID-19 pandemic such as worker shortages and raw material bottlenecks continue to pose operational challenges. To navigate these challenges, manufacturers need to focus on diversifying their supply chain networks and sourcing raw materials from multiple regions. They also need to consider expanding production capacities in other low-cost emerging markets to reduce over-reliance on Europe and minimize disruptions. Adopting advanced technologies for improving productivity and yield can help optimize costs as well. Partnerships with distributors and retailers assume more importance for sustainably catering to demand pockets. Overall, strategizing innovations, building resilient operations, and exploring new markets will be vital for achieving long-term goals amid geopolitical volatility. The food grade alcohol market in terms of value is currently concentrated in Europe, with countries like Germany, France, UK among the top consumers. This is attributed to robust demand from the beverage, food processing, and pharmaceutical industries in the region. However, Asia Pacific is emerging as the fastest growing regional market owing to rising health consciousness, growing disposable incomes, and expanding applications in personal care and cosmetic products sectors across countries like China, India, Japan and South Korea. Demand from Asia Pacific is expected to outpace others over the coming years. The food grade alcohol market in Asia Pacific is witnessing strong growth currently, driven by increasing health awareness among consumers and a booming beverages industry. China dominates the regional market and will continue exhibiting high growth. However, India is poised to be the fastest growing market during the forecast period, supported by a burgeoning middle class, rising alcohol consumption, and augmenting demand for hand sanitizers and disinfectants post COVID-19. Furthermore, expanding food processing, personal care, and pharmaceutical sectors will further support market prospects across other high-potential Asian countries. Get more insights on This Topic- Food Grade Alcohol Market Skin Rash Treatment Market Is Growing Rapidly With Rising Adoption Of Home-Based Therapies4/24/2024  Skin Rash Treatment Market The skin rash treatment market comprises products such as topical corticosteroids, antihistamines, pruritus therapeutics, antibiotics and antifungals which are used to treat various skin rashes. These products provide immediate relief from the itching, swelling and redness caused by rashes. Topical corticosteroids are the most commonly used products for rash treatment due to their fast symptom relief. Growing preference for home-based therapies to self-treat minor rashes is fueling the demand for over-the-counter skin rash treatment products.

The Global Skin Rash Treatment Market is estimated to be valued at US$ 3.67 BN in 2024 and is expected to exhibit a CAGR of 6.5% over the forecast period 2024 to 2031. Market Key Trends Rising adoption of home-based therapies is a key trend being witnessed in the Skin Rash Treatment Market Size. Growing preference for self-medication to treat minor skin disorders at home has increased the demand for over-the-counter topical creams and ointments. Manufacturers are launching small packaged and affordable products specifically designed for home use. Introduction of advanced formulations such as gel-based and soap-free products is also increasing their popularity in the home therapy segment. Rising internet and smartphone penetration has further enabled consumers to purchase skin rash treatment kits and creams online from the comfort of their homes. Key Takeaways Key players operating in the skin rash treatment market are AbbVie, Amgen, Bristol Myers Squibb, Galderma, Johnson & Johnson, LEO Pharma, Merck & Co. Inc., Novartis AG, Pfizer Inc., Sanofi, Sun Pharmaceutical Industries Pvt. Ltd., Teva Pharmaceutical Industries, Valeant Pharmaceuticals, Mylan N.V., Perrigo Company plc, and Eli Lilly and Company. The growing prevalence of skin disorders caused due to pollution, changing lifestyle and dietary habits has increased the demand for skin rash treatment products. Rising awareness regarding personal care and availability of these products through online channels is fueling the growth of the global skin rash treatment market. Growing demand in emerging economies of Asia Pacific and Latin America has prompted companies to expand their business operations in these regions. The increasing middle-class population and healthcare expenditures in countries like India, China, Brazil and Mexico have significantly boosted the sales of skin rash treatment products. Rising awareness programs by government organizations regarding personal health and hygiene are further strengthening the market growth. Porter's Analysis Threat of new entrants: The skin rash treatment market has moderate threat of new entrants as it requires large investments for R&D, clinical trials and production facilities. However, new targeted therapies offer opportunities. Bargaining power of buyers: The bargaining power of buyers is moderate given the availability of generic substitutes and focus on value-based pricing. Large healthcare organizations are able to negotiate on price and convince patients to use economical generic alternatives. Bargaining power of suppliers: The bargaining power of suppliers is low to moderate asraw material inputs are available from multiple suppliers. However, suppliers of innovative drugs hold some power. Threat of new substitutes: The threat of substitutes is moderate as newer targeted therapies offer possibilities. However, an established body of clinical evidence favors existing options over substitutes. Competitive rivalry: The competition in the market is high among major global players offering varied products. Geographical regions: North America accounts for approximately 40% value share of the global skin rash treatment market, led by the U.S. due to higher per capita healthcare spending and rapid adoption of advanced therapies. Fastest growing region: Asia Pacific region is poised to witness the fastest growth during the forecast period, increasing at a CAGR of over 8%, with major markets including China and India contributing to growth. This is attributed to rising income, growing medical tourism, and increasing healthcare expenditures. Explore More Articles- Topical Drug Delivery Market  Global Tattoo Aftercare Products Market The global tattoo aftercare products market involves a variety of products aimed at assisting tattoo healing and proper care. Tattoo aftercare products include creams, gels, and moisturizers that contain antimicrobial properties and aim to hydrate, heal, and protect new tattoos. Tattoo aftercare allows reducing risk of infection, alleviating pain and discomfort, and promoting long-lasting ink quality by caring for tattoos during the healing process. The rising number of people adorning tattoos, especially among millennials, has boosted demand for aftercare products.

The Global Tattoo Aftercare Products Market is estimated to be valued at US$ 194.1 MN in 2024 and is expected to exhibit a CAGR of 9.6% over the forecast period 2024 To 2031. Key players operating in the global tattoo aftercare products market are TATWAX, INKEEZE, INC., DISCOVERWOO, Tattoo Goo, LLC., Lubriderm, Aussie Inked, Helios Tattoo, SORRY MOM, Born4design Ltd., SKINFIX INC., W. S. Badger Company, H2Ocean, and Mad Rabbit. Key Takeaways Key players: Key players operating in the Global Tattoo Aftercare Products Market Size are focusing on product innovation and expanding their distribution channels. For instance, TATWAX specializes in natural plant-based aftercare products. INKEEZE, INC. offers alcohol-free aftercare sprays and ointments. Growing demand: Rising cultural acceptance of tattoos and growing millennials population are fueling the demand for aftercare products. Increase in small tattoos and home tattooing during the pandemic has also boosted the need for proper care of new ink. Global expansion: Leading companies are expanding their geographical footprints to capitalize on opportunities in developing countries witnessing surge in tattoo practices. DISCOVERWOO entered international markets like Australia and New Zealand. Lubriderm has worldwide availability in over 60 countries. Market key trends The use of natural and organic ingredients in aftercare products is a key trend in the tattoo aftercare products market. Players are focusing on developing ingredients sourced from plants, herbs and other natural sources to cater to consumer demand for chemical-free products. For instance, TATWAX uses grapeseed oil, aloe vera and lavender extracts in its aftercare range. This trend allows soothing tattoos naturally during healing without risk of side-effects. Porter's Analysis Threat of new entrants: The Tattoo Aftercare Products Market faces moderate threat as market has few major players however establishing a brand is challenging. Bargaining power of buyers: Buyers have moderate bargaining power as there are substitutes available however dedicated tattoo aftercare brands have loyal customer base. Bargaining power of suppliers: Suppliers have low bargaining power as raw materials used in tattoo aftercare products are widely available. Threat of new substitutes: Threat of new substitutes is low as existing brands have strong brand equity however hand sanitizers and moisturizers can act as substitutes. Competitive rivalry: The market sees intense competition between major brands to enhance their market share through new product offerings. Geographical Regions North America region accounts for the largest share in the global Tattoo Aftercare Products market in terms of value owing to increasing tattoo culture and growing millennials population in the region. The region constitutes over 35% share of the global market. Asia Pacific region is expected to witness the fastest growth during the forecast period owing to rising per capita incomes, growing middle class population and increasing youth population opting for tattoo trends in countries like India and China. The region is expected register a CAGR of over 12% during the forecast period. Explore More Articles - Global Agrigenomics Market  Market Drivers

The Low Profile Additives Market is witnessing significant growth driven by several key factors. One of the primary drivers is the increasing demand from industries such as automotive, construction, and aerospace for lightweight materials with enhanced performance properties. Low profile additives play a crucial role in improving the mechanical strength, durability, and surface finish of composite materials, thereby meeting the stringent requirements of these industries. Additionally, the growing emphasis on sustainability and environmental regulations is driving the adoption of low profile additives as they enable the production of eco-friendly and recyclable composite materials. These factors collectively underscore the importance of the Low Profile Additives Market in facilitating technological advancements and innovation in various end-use applications. The Low Profile Additives Market size was valued at US$ 760.3 Million in 2023 and is expected to reach US$ 1,247.9 Million by 2031, growing at a compound annual growth rate (CAGR) of 6.4% from 2024 to 2031. Key players operating in the Low Profile Additives Market Wacker Chemie AG, INEOS AG, Polynt S.p.A., Vin Industries, BASF SE, Altana, Polychem Ltd., Swancor, LyondellBasell Industries Holdings B.V., Aromax Technology Corp., Interplastic Corp., Synthomer PLC, AOC, LLC, Mechemco, Taak Resin Co., NOF Corporation. PEST Analysis A PEST analysis offers insights into the macro-environmental factors shaping the Low Profile Additives Market Size. Political stability and government regulations influence market dynamics by impacting trade policies, environmental regulations, and funding initiatives for research and development in the composite materials industry. Economic factors such as fluctuating raw material prices and currency exchange rates affect production costs and profitability for market players. Moreover, social factors, including consumer preferences for sustainable products and awareness about environmental conservation, drive market demand for low profile additives. Technological advancements and innovations in manufacturing processes further propel market growth, enhancing the efficiency and performance of low profile additives in the production of composite materials. SWOT Analysis The SWOT analysis provides a comprehensive understanding of the strengths, weaknesses, opportunities, and threats facing the Low Profile Additives Market. Strengths lie in the versatility and effectiveness of low profile additives in improving the mechanical properties and surface finish of composite materials. Moreover, the increasing demand for lightweight and high-performance materials in various industries presents opportunities for market expansion and revenue growth. Weaknesses may include the dependency on raw material availability and the need for continuous innovation to meet evolving customer requirements. Additionally, competitive pressures and price fluctuations pose challenges for market players operating in the Low Profile Additives Market. Despite challenges, opportunities abound in the Low Profile Additives Market, driven by technological advancements and growing applications in end-use industries such as automotive, construction, and marine. Market expansion opportunities are particularly evident in emerging economies with rapid industrialization and infrastructure development. Furthermore, strategic partnerships and collaborations among manufacturers, suppliers, and end-users facilitate market penetration and product development. The integration of advanced technologies, such as nanotechnology, in the formulation of low profile additives holds promise for enhancing performance properties and creating value-added solutions for customers in the Low Profile Additives Market. The Low Profile Additives Market is poised for significant growth driven by various market drivers, including the increasing demand for lightweight and high-performance materials across industries. A PEST analysis highlights the macro-environmental factors shaping market dynamics, while a SWOT analysis offers insights into the market's strengths, weaknesses, opportunities, and threats. Despite challenges, opportunities abound in emerging economies and technological innovations, positioning the Low Profile Additives Market for sustained growth and innovation in the years to come. Explore More Articles – Global In Vitro Lung Model Market  Butylated Hydroxytoluene Market Butylated hydroxytoluene (BHT) is a lipophilic organic compound and a phenolic antioxidant which is widely used to prevent the oxidation of fats and therefore food deterioration. It helps increase the shelf life of food products. BHT is used as a food additive and preservative in packaged foods, animal feeds, cosmetics, food packaging, rubber, petroleum products and related materials. BHT acts as a radical scavenger to inhibit the chain reaction of autoxidation. It reacts with the free radicals formed in the initiation step and converts them into more stable products.

The Global Butylated Hydroxytoluene Market is estimated to be valued at US$ 236.8 MN in 2024 and is expected to exhibit a CAGR of 5.6% over the forecast period 2024 to 2031. Growing awareness about harmful effects of oxidation and deteriorated quality of food products has fueled the demand for antioxidants like BHT. Increasing production of packaged and processed foods has also augmented the market growth due to longer shelf life requirement of foods. Moreover, rising consumption of personal care products and cosmetics is propelling the BHT consumption. Key Takeaways: Key players operating in the Butylated Hydroxytoluene market are Oxiris Chemicals S.A., Camlin Fine Science, Finoric LLC, Dycon Chemicals, Honshu Chemical Industry Co., Ltd., Sasol Limited, Lanxess, Eastman Chemical Company. Growing concerns about food safety and quality has increased the demand for effective food preservatives like BHT globally. Asia Pacific region dominates the global demand for BHT due to enormous food processing industry. Major players are focusing on global expansion plans by acquiring small players and setting up production facilities in high growth regions. The Butylated Hydroxytoluene market has high opportunities in developing nations to meet the rising demand from food and personal care sectors. Market key trends: One of the key trends observed in the Butylated Hydroxytoluene Market Size is increasing applications in food packaging materials. Traditionally, BHT was only used in direct food contact application but now it is extensively utilized as an antioxidant for food packaging films and containers. This helps increase the shelf life of packaged foods. Growing focus on freshness and quality of packaged foods is augmenting the demand for BHT from food packaging sector. Porter's Analysis Threat of new entrants: New manufacturers find it difficult to enter this market as it requires high capital investment in research and development activities and also existing manufacturers have strong brand loyalty. Bargaining power of buyers: Buyers have low bargaining power in this market as it is commodity chemical with limited substitutes and manufacturers differentiate their products on trademark basis. Bargaining power of suppliers: Suppliers have moderate bargaining power as raw materials for BHT production such as cumene and phenol derivatives are widely available from various international suppliers. Threat of new substitutes: Threat of substitutes is moderate as some alternatives like TBHQ and synthetic antioxidants are used but they are costly and may not provide same level of performance as BHT. Competitive rivalry: Competition in the market is high as top players aggressively compete on pricing, quality and brand loyalty while expanding capacities to gain higher market share. Geographical Regions North America region accounted for largest share in the global BHT market in terms of value owing to wide usage of BHT in food, pharmaceuticals, polymers and fuel additives industries in US and Canada. Asia Pacific region is expected to be the fastest growing market during forecast period supported by rising demands from food packaging, plastics and fuel additive end use industries in China, India and other Southeast Asian countries. The BHT market in Europe is mainly concentrated in Western European countries like Germany, UK, France and Italy where stringent food safety regulations mandate usage of antioxidants in processed food products. Japan is also a major consumer market in Asia Pacific region due to high living standards and aging population demanding preservation of food quality. Explore More Articles - Global Space Situational Awareness (SSA) Market  Vehicle Protection Service Market In the realm of automotive services, the Vehicle Protection Service Market stands as a pivotal segment, offering comprehensive solutions to safeguard vehicles against various risks and uncertainties. This market is propelled by several key factors, shaping its trajectory and influencing its growth dynamics. Understanding these drivers is essential for stakeholders to navigate the landscape effectively.

The Global Vehicle Protection Service Market size is estimated to be valued at US$ 146.01 Bn in 2023 and is expected to reach US$ 288.3 Bn by 2030, grow at a compound annual growth rate (CAGR) of 10.2% from 2023 to 2030. Key players operating in the Vehicle Protection Service Market Endurance Warranty Services LLC, CarShield, Protect My Car, Ally Financial Inc., CARCHEX, Toco Warranty, American Auto Shield, Warranty Direct, Royal Administration Services, Inc., EasyCare (Automotive Development Group, Inc.), Autopom!, AA Auto Protection, and CarSure One of the primary drivers bolstering the Vehicle Protection Service Market Size is the escalating demand for extended warranty and maintenance plans. As vehicle ownership costs continue to rise, consumers are increasingly seeking ways to mitigate the financial risks associated with unexpected repairs and damages. Consequently, the market witnesses a surge in the adoption of vehicle protection services, as they offer peace of mind and financial security to vehicle owners. Moreover, the proliferation of advanced automotive technologies further augments the demand for vehicle protection services. Modern vehicles are equipped with sophisticated electronics and complex mechanical components, rendering them susceptible to malfunctions and breakdowns. As a result, consumers are inclined towards investing in comprehensive protection plans offered by Vehicle Protection Service Market players, ensuring timely repairs and maintenance to uphold the performance and longevity of their vehicles. Conducting a PEST analysis unveils the external factors shaping the Vehicle Protection Service Market landscape. Political stability and regulatory frameworks play a crucial role in determining the market dynamics. Government initiatives promoting consumer rights and vehicle safety standards influence the market's operational landscape, fostering transparency and accountability among service providers. Economic factors, including disposable income levels and consumer spending patterns, significantly impact the market's growth trajectory. In times of economic prosperity, consumers exhibit a higher propensity to invest in vehicle protection services, viewing them as essential safeguards against unforeseen expenses. Conversely, during economic downturns, demand may experience a temporary slowdown, prompting market players to devise innovative pricing strategies and value-added offerings to maintain competitiveness. From a socio-cultural perspective, evolving consumer preferences and lifestyle trends influence the market's evolution. The growing emphasis on convenience and personalized experiences drives the demand for tailored protection plans that cater to diverse customer needs. Additionally, the increasing awareness regarding environmental sustainability prompts the emergence of eco-friendly vehicle protection solutions within the Vehicle Protection Service Market, aligning with shifting consumer values and preferences. A comprehensive SWOT analysis offers strategic insights into the Vehicle Protection Service Market, delineating its internal strengths and weaknesses, as well as external opportunities and threats. Market incumbents leverage their established brand reputation and extensive service networks as key strengths, fostering customer trust and loyalty. Furthermore, strategic partnerships with automotive manufacturers enable service providers to offer integrated protection solutions, enhancing their market presence and competitiveness. However, challenges such as pricing pressures and regulatory compliance pose significant hurdles for Vehicle Protection Service Market players. Intensifying competition and commoditization within the market compel service providers to innovate and differentiate their offerings to maintain profitability and sustain growth. Moreover, evolving consumer preferences and technological advancements necessitate continuous adaptation and investment in R&D to stay ahead of the curve. Amidst these challenges, the Vehicle Protection Service Market presents lucrative opportunities for expansion and diversification. With the rising adoption of connected vehicles and telematics technologies, service providers can leverage data-driven insights to offer predictive maintenance and real-time diagnostics, enhancing the overall customer experience. Additionally, expanding into emerging markets and untapped customer segments presents avenues for sustainable growth and market penetration. The Vehicle Protection Service Market is propelled by various drivers, including the demand for extended warranty plans and advancements in automotive technologies. Conducting a comprehensive PEST and SWOT analysis unveils the market's external influences and internal dynamics, guiding stakeholders in formulating strategic decisions and capitalizing on growth opportunities within this dynamic and evolving landscape. Explore More Articles – Global Multiomics Market |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

April 2024

Categories |

RSS Feed

RSS Feed