Polycarbonate Market Polycarbonate or polycarbonate (PC) plastic is a transparent thermoplastic with many applications in eyewear, medical devices, automotive interiors, consumer electronics, food and beverage containers etc owing to its impact resistance, heat resistance and optical transparency. It is 20 times stronger than glass and is four times lighter, as well as being transparent, heat resistant and able to be molded into various shapes.

The Global Polycarbonate Market is estimated to be valued at US$ 186.71 Bn in 2024 and is expected to exhibit a CAGR of 10% over the forecast period 2024 to 2030. Key Takeaways Key players operating in the Polycarbonate Market Size are Acadian Seaplants Limited, Biostadt India Limited, Omex Agrifluids Ltd., Italpollina Spa, Koppert B.V., Bio Atlantis Ltd., Platform Specialty Products Corporation, BASF SE, Novozymes A/S, Agrinos A/S. Key players are focusing on development of sustainable and recyclable polycarbonate materials to cater to the increasing demand for eco-friendly products. The increasing demand for lightweight and high-performance polymers from automotive and construction industries is driving the growth of the global polycarbonate market. Also, growth of electronic industry is propelling the market growth as polycarbonate provides shatter resistance and durability required for various electronic parts. The global polycarbonate market is expanding significantly with growing demand from emerging economies of Asia Pacific led by countries like China and India. Also, recovering automotive production in Europe and North America is contributing to the regional market growth. Market Key Trends Recyclability of polycarbonate plastic through mechanical recycling is one of the key trends in the market. Major players are focusing on closed loop recycling initiatives to recover polycarbonate from various waste streams to manufacture new products, in line with sustainability goals. Also, bio-based or plant-based polycarbonate materials developed from renewable resources like vegetable oils are gaining popularity as an alternative to conventional polycarbonates to reduce dependency on fossil fuels. Porter’s Analysis Threat of new entrants: Low economies of scale in production and high capital requirements make it difficult for new players to enter the market. Bargaining power of buyers: Buyers have moderate bargaining power due to availability of substitutes and differentiated products from various manufacturers. However, presence of large established buyers decreases their bargaining power. Bargaining power of suppliers: Suppliers may have moderate bargaining power due to availability of raw material alternatives and global presence of established raw material suppliers. Threat of new substitutes: Threat is moderate as substitute products like glass and metal offer similar properties for some applications. Competitive rivalry: Intense as major players compete on pricing, quality improvement and new product development through R&D investments. Geographical Regions The Asia Pacific region accounted for the largest share in the global polycarbonate market in terms of value in 2019. China dominates the Asia Pacific polycarbonate market owing to the presence of tier-1 manufacturers as well as increasing demand from the electrical and electronics, automotive, medical devices and construction industries in the country. North America is the second-largest market for polycarbonate globally, attributed to the high and growing demand from various end-use industries such as electrical and electronics, automotive, consumer goods and medical devices. Europe is expected to exhibit the fastest growth during the forecast period owing to high demand for polycarbonate resins in electrical and electronics, medical devices and automotive applications. Additionally, recovery in the automotive industry is also anticipated to propel the market growth in Europe over the next few years. In terms of value and volume, developing countries of Latin America and Middle East & Africa are projected to witness above-average growth in demand for polycarbonate from 2024 to 2030 compared to other regions attributed to ongoing industrialization and infrastructure development activities. Get more insights on- Polycarbonate Market

0 Comments

Police Baton Market The Police baton market comprises expandable batons, straight batons, and other batons that are used for law enforcement and riot control purposes. Police batons provide law enforcement agencies a flexible and non-lethal weapon option to de-escalate situations and ensure public safety without inflicting serious harm. The demand for police batons is increasing owing to growing investments in improving law enforcement capabilities globally.

The Global Police Baton Market is estimated to be valued at US$ 158.06 Bn in 2024 and is expected to exhibit a CAGR of 14% over the forecast period 2024 to 2030. Key Takeaways Key players operating in the Police baton market are BASF SE, Braskem S.A., Koninklijke DSM N.V., Arkema S.A., Innovia Films. Ltd., Metabolix, Inc., NatureWorks, LLC, Novamont S.p.A., and The Dow Chemical Company. These players are focusing on developing innovative baton designs for improved safety, control, and damage mitigation. The police baton market provides significant opportunities for players involved in research & development of batons made from lightweight and sustainable materials. Innovation in baton designs can help address changing law enforcement requirements and minimize risks of injuries. The demand for police batons is increasing globally with law enforcement agencies around the world investing in equipping their forces adequately. Key players are expanding their international operations to leverage opportunities in emerging markets such as Asia Pacific and Middle East & Africa. Market drivers - Increasing investments by governments globally to modernize law enforcement capabilities is a key factor driving the demand for police batons. This is enabling procurement of non-lethal weapons for crowd control and rioting situations. - Growing concerns over public safety and focus on minimizing human casualties during law and order operation is also propelling the need to adopt efficient crowd control mechanisms including police batons. Market restraints - High costs associated with procurement of advanced baton technologies may limit widespread adoption, especially in budget constrained law enforcement set ups in developing regions. - Stringent regulations and oversight on procurement and use of police batons in some countries may additionally challenge sales up to a certain extent. Segment Analysis Police Baton Market Size can be broadly categorized into wooden batons, metal batons, and composites batons. Wooden batons dominate the market currently. They are preferred due to their lightweight and ability to cause medium intensity blows. However, they cannot withstand high impact blows and have a risk of breakage. Metal batons are second largest segment. They are heavier but can withstand high impact blows making them suitable for riot control purposes. However, they pose higher risks of injury. Composites batons segment is growing at fastest rate as they combine advantages of both wooden and metal batons. They are lightweight, withstand multiple impacts, and have low risk of injury. Composites baton segment is expected to be the dominating segment going forward. Global Analysis North America currently dominates the global police baton market with United States being the major market. High funding for law enforcement combined with periodic upgradation of equipment drives the North America market. Asia Pacific is the fastest growing region globally. Increasing police modernization programs and growing investment in training and equipment in major Asia Pacific countries such as China and India is contributing to the growth. The region is expected to surpass North America to become the dominating regional market by 2030 due to high economic growth and rising focus on public security in developing Asian countries. Europe is another major regional market but growth is slower compared to Asia Pacific. Get more insights on- Police Baton Market  Photomedicine which is technology enabled application of light in medicine is increasingly becoming popular for personalized treatment. Photomedicine involves technologies like laser, LEDs and broadband light sources as therapies for various conditions. Photomedicine allows non-invasive or minimally invasive procedures for conditions like acne, wrinkles, pigmentation, hair removal, tattoo removal and much more. The growing preference for personalized and minimal intervention treatment is driving increased adoption of photomedicine.

The Global Photomedicine Market is estimated to be valued at US$ 4.15 Bn in 2024 and is expected to exhibit a CAGR of 5.9% over the forecast period 2024 to 2030. Photomedicine offers advantages like precision, effectiveness and reduced risks of side effects over conventional medication in many cases. Development of advanced light devices and increasing acceptance of aesthetic applications are creating significant need for photomedicine based products and services. Key Takeaways Key players operating in the Photomedicine market are Bombay Spirits Company LTD, Diageo plc, William Grant & Sons Ltd, Charles Tanqueray & Co., Vantguard, Jaisalmer Indian Craft Gin, Nao Spirits & Beverages Pvt Ltd, Radico Khaitan Limited, Pernod Ricard, and Beam Suntory, Inc. The growing use of photomedicine in applications like tattoo removal, acne treatment, hair removal, skin resurfacing and skin therapy is fueling the demand for photomedicine products and technologies. Improving economic conditions and increasing income levels are enabling people to spend more on personal care and aesthetic treatments globally. Increasing awareness about minimally invasive procedures and growing medical tourism are driving international expansion of photomedicine market players. Establishment of production and treatment facilities across major global markets allows companies to capture the growing demand. Market key trends Use of combination technologies in Photomedicine Market Size is a key trend. Combining different light modalities like lasers, LEDs and broadband light allows more effective and customized treatment. Another trend is development of home use photomedicine devices for applications like acne, hair removal, wrinkle reduction etc. This is increasing access and convenience. Advances in light delivery systems through innovative optical fibers, handpieces are also improving treatment outcomes. Porter's Analysis Threat of new entrants: New entrants face high initial costs for R&D and setting up manufacturing facilities. Bargaining power of buyers: Buyers have moderate bargaining power due to availability of substitute treatments. Bargaining power of suppliers: Suppliers have low to moderate bargaining power as there are many component manufacturers. Threat of new substitutes: Substitute treatments like medicine and surgery provide competition. Competitive rivalry: High among existing players. Geographical Regions North America holds the largest share of the photomedicine market owing to presence of developed healthcare infrastructure and high adoption of novel technologies. Asia Pacific region is poised to grow at the fastest CAGR during the forecast period due to increasing medical tourism, rising healthcare expenditure and growing geriatric population. Geographical Regions The United States accounts for the major share of the North American photomedicine market due to availability of advanced healthcare facilities and favorable reimbursement policies. China dominates the Asia Pacific region and is expected to witness exponential growth supported by improving healthcare infrastructure, mounting medical tourism and rising disposable incomes. Get more insights on- Photomedicine Market  Pharmaceutical Traceability Market The pharmaceutical traceability market involves tracking drugs from the point of manufacturing to the point of dispensing. Traceability equipment helps verify the authenticity of drugs and identify counterfeits. Barcode printers, labeling and serialization machines, and verification equipment are widely used. The need for traceability has grown due to rising instances of counterfeit drugs and stringent regulations. The EU Falsified Medicines Directive requires unique identification codes on drug packs. Similarly, the U.S. Drug Supply Chain Security Act mandates tracing pharmaceuticals using serialization.

The Global pharmaceutical traceability market is estimated to be valued at US$ 4.96 Bn in 2024 and is expected to exhibit a CAGR of 9.5% over the forecast period 2024 to 2030. Key Takeaways Key players: Key players operating in the Pharmaceutical Traceability Market Size include M&R Printing Equipment, MHM Siebdruckmaschinen GmbH, Lawson Screen & Digital Products, Sakurai USA, SPS TechnoScreen GmbH, ATMA Champ Ent. Corp., Systematic Automation, DECO TECHnology Group, TOSH (Italy), and Thieme GmbH & Co. KG. Key opportunities: The market provides opportunities for players dealing with serialization and aggregation equipment, used to bundle drugs together and assign unique identifiers. Cloud-based track and trace solutions are also gaining attention to monitor pharmaceuticals across international borders. Global Expansion: Major manufacturers are expanding globally to cater to the growing demand for traceability from companies operating worldwide. For example, some players have set up production sites and local offices in Europe, Asia, and North America to serve local customers better. Market drivers: Stringent regulations mandating drug traceability from manufacturing to the consumer are a key driver for this market. Regulations ensure quality and limit counterfeiting activities. Authentication technology advances are also fueling the adoption of track and trace solutions. Market restraints: High costs of traceability equipment and ongoing upgrades could challenge smaller pharmaceutical firms. Additionally, the lack of a globally harmonized framework for drug traceability remains a hurdle to cross-border trades. This restrains full implementation and scope for global connectivity solutions. Segment Analysis The Pharmaceutical Traceability Market can be segmented based on several product types such as serialization solutions, aggregation solutions, and tracking, tracing, and reporting solutions. The serialization solutions segment currently dominates the market due to stricter serialization regulations and deadlines introduced by various regulatory bodies globally to uniquely identify pharmaceutical products and combat counterfeiting. These solutions offer serialization at the unit or carton level to help organizations comply with regulations. Global Analysis Regionally, North America holds the major share in the Pharmaceutical Traceability Market due to stringent regulations enforced by the FDA in the region. The FDA requires all pharmaceutical manufacturers in the US to implement product serialization at the unit level by November 2023. However, the market in Asia Pacific is expected to grow at the highest CAGR during the forecast period due to the growing generics market and implementation of track and trace systems by developing countries such as India and China. Key players in the market focus on geographic expansion opportunities across Asia Pacific and Latin America to strengthen their global presence. Get more insights on- Pharmaceutical Traceability Market  As environmental concerns continue to rise, businesses and consumers are searching for more sustainable options. One area ripe for innovation is packaging materials. Traditionally, foam products like cushions, packaging peanuts, cups and plates have used petroleum-based plastics that do not break down over time and end up polluting the earth. However, new biodegradable foams are emerging as a green alternative.

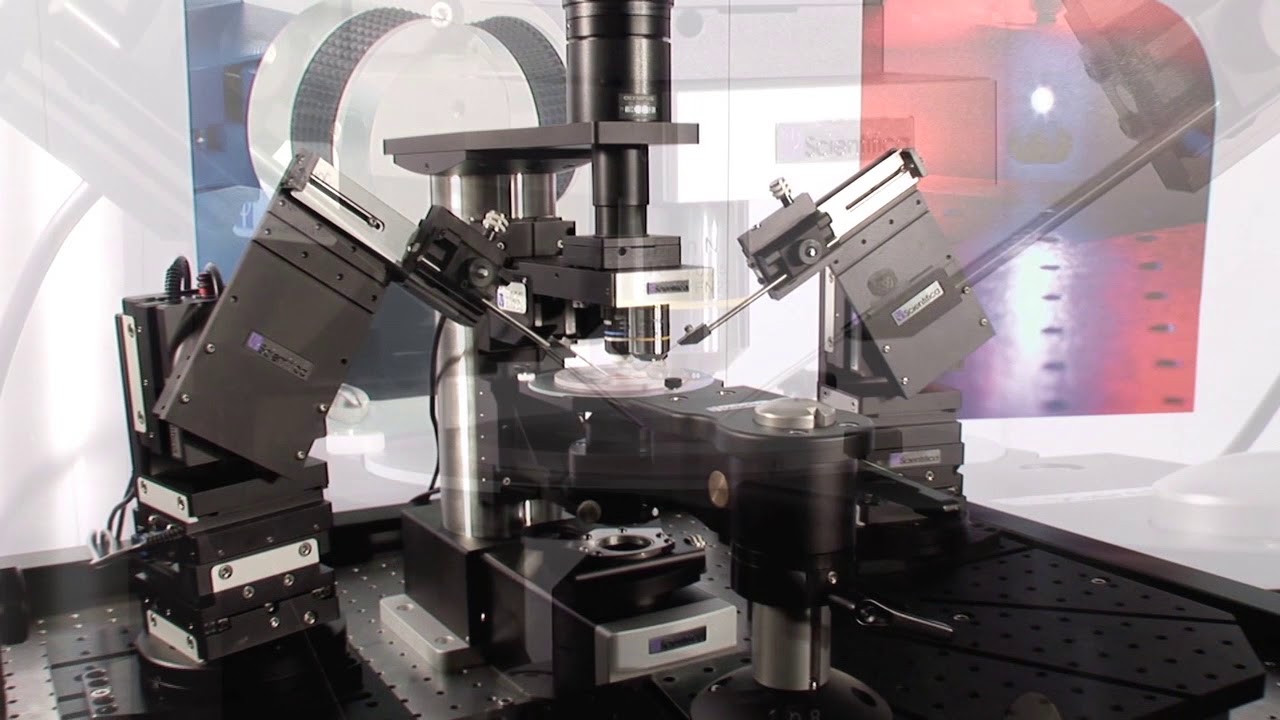

What is Biodegradable Foam? Biodegradable foam is made from renewable, plant-based materials instead of petroleum. The two main types are: - Starch-based foams: These foams use corn, potatoes or other starches as the raw material. The starches are mixed with modifiers and blowing agents to create a lightweight, insulating foam structure. Key characteristics include sustainability, moisture absorption and compostability. - Polylactic acid (PLA) foams: PLA is a bioplastic derived from corn or sugarcane. It can be processed into foam using physical blowing agents. PLA foams are rigid yet brittle compared to traditional petroleum foams. They also have a higher melting point and slower decomposition rate. Both starch-based and PLA foams fully break down when exposed to moisture, oxygen, sunlight and microorganisms. This allows them to safely decompose in compost piles or landfills without polluting the environment long-term. Applications of Biodegradable Foam Biodegradable foams are now used across many industries as a green substitute for petroleum foams. Some key applications include: - Packaging: Companies use biodegradable foam peanuts, sheets and molded shapes to cushion, separate and fill spaces in shipments of goods. This keeps products protected without creating long-lasting waste. - Food packaging: Foam cups, plates, clamshell containers and eating utensils made from PLA or starch are popular for single-use applications at events and restaurants. They decompose easily after use. - Furniture: Cushions, mattresses and seat cushions made with biodegradable foam allow furniture to have a softer feel while lowering environmental impact at end of life. - Automotive: Biodegradable foam insulation allows car manufacturers to meet emission standards while ensuring materials break down safely. It also cushions interiors during impacts. - Construction: Biodegradable spray foam is used for insulation, soundproofing, and to fill cracks and gaps in buildings. It provides the required performance without harming ecosystems long-term. Benefits of Using Biodegradable Foams Switching to biodegradable foam solutions offers numerous advantages for businesses and the planet: Sustainability - By using plant-based feedstocks instead of petroleum, biodegradable foams have a much lower carbon footprint over their lifecycle. They also avoid filling fragile landfills long-term. Reduced waste - Since these foams fully decompose, there is no toxic foam waste left behind. This cuts cleanup and disposal costs versus traditional foams. Renewability - Resources like corn, potatoes and sugarcane can be replenished annually, ensuring a steady supply of raw materials now and in the future. Performance parity - Formulation advancements have allowed Biodegradable Foam to closely match the insulation, impact resistance and other properties of petroleum versions. Positive brand perception - Consumers are actively seeking out eco-friendly products. Using biodegradable foams builds goodwill and enhances a company's environmental reputation in the market. Government support - Many governments now offer procurement preferences or incentives for using renewable, biodegradable materials in industries like construction and packaging. Room for Improvement While biodegradable foams have made great strides, further refinement is still needed to address some limitations: Cost - Production costs remain 10-30% higher than petroleum foams currently. Increased manufacturing volumes could lower this gap over time. Decomposition times - Complete degradation of some biodegradable foams may take over 6 months depending on composting conditions, versus mere days for others. Performance at extremes - High/low temperature resistance as well as long-term durability need more enhancement versus petroleum-based competitors. Standardization - Agreeing upon globally recognized compostability/biodegradability certifications and test methods will boost market adoption. Overall, biodegradable foam shows excellent potential as a sustainable replacement for many traditional petroleum foams. With continued development efforts, it could become the new standard across various industries seeking greener solutions. Both businesses and the planet stand to benefit in the long run. Get more insights on- Biodegradable Foam  Automated Patch Clamp System Market Automated patch clamp systems help generate high-quality electrophysiological data from ion channels and receptors with high throughput screening capabilities. The precise recordings obtained from automated patch clamp systems enable accurate drug screening and ion channel research.

The global automated patch clamp system market is estimated to be valued at US$ 579.83 Mn in 2024 and is expected to exhibit a CAGR of 6.0% over the forecast period from 2024 to 2030. Key Takeaways Key players operating in the automated patch clamp system market are GE Healthcare, Siemens Healthineers, Philips Healthcare, Toshiba Medical Systems Corporation, Hitachi Healthcare, Canon Medical Systems Corporation, Mindray Medical International Limited, Esaote SpA, NeuroLogica Corporation, NeuroVive Pharmaceutical AG, Brainlab AG, Akili Interactive Labs Inc., Brainomix Ltd., Imaging Science International, Mevis Medical Solutions, NeuroVista, Neusoft Medical Systems, Positron Corporation, Shimadzu Corporation, Trifoil Imaging. Growing demand for ion channel screening in drug discovery and the increasing research activities in neuroscience are fueling the growth of the global automated patch clamp system market. In addition, the rising collaboration between research institutes and key market players for development of advanced automated patch clamp systems for high throughput screening is strengthening the growth of the market. Furthermore, expanding geographical presence of major market players through new product launches and strategic partnerships in emerging markets like Asia Pacific and Latin America is expected to offer lucrative growth opportunities for the market during the forecast period. Market key trends Adoption of high throughput screening with automated patch clamp systems for ion channel drug screening is one of the key trends witnessed in the market. High throughput screening allows screening of thousands of compounds in a short period of time which aids in accelerating the drug discovery process. Another major trend is the increasing preference towards miniature automated patch clamp systems due to their compact size and portability. Miniaturized patch clamp systems enable researchers to conduct electrophysiology experiments outside the laboratory setup with ease. Ongoing technological advancements including incorporation of AI and machine learning capabilities in automated patch clamp systems for data analysis is expected to drive innovations and expand the application scope of these systems in the coming years. Porter’s Analysis Threat of new entrants: The Automated Patch Clamp System Market Size requires huge capital investments and established distribution channels. Additionally, the presence of major players makes it difficult for new entrants to acquire sufficient market share. Bargaining power of buyers: Large healthcare facilities and research organizations have greater bargaining power due to high purchase volumes. However, the need for advanced medical devices limits the impact of buyer power. Bargaining power of suppliers: Major suppliers in the market include semiconductor companies and device component manufacturers. Supplier power is moderate as there are many alternatives. Threat of new substitutes: There are limited substitutes for automated patch clamp systems due to their unique ability to study ion channel behavior. However, alternative testing techniques pose a minor threat. Competitive rivalry: The market features the presence of many global and regional providers. Players compete based on product features, pricing, and service/support. Geographical Regions North America currently holds the largest share of the automated patch clamp system market due to increased adoption, technological advancements, and rising healthcare expenditure. The Asia Pacific region is expected to grow at the fastest pace during the forecast period driven by improving access to healthcare facilities, rising medical tourism, and growing geriatric population. Automated patch clamp systems help electrophysiologists and neuroscientists characterize ion channels and provide critical data for drug discovery and development. Some key applications include drug safety profiling, drug discovery, drug screening, toxicology, and basic research. GE Healthcare, Siemens Healthineers, and Philips Healthcare are major providers catering to the needs of hospitals, academic institutes, and pharmaceutical companies globally. Get more insights on- Automated Patch Clamp System Market  The Automated Fiber Placements And Automated Tape Laying Machines Market comprise machines that automate the process of laying fiber composites and tapes on molds to manufacture composite parts. Automated fiber placement machines work on the same basic principle as automated tape laying machines but use smaller, multidirectional fiber tows instead of prepreg tape. These machines help reduce labor cost and enhance productivity by automating the composite layup process.

The Global automated fiber placements and automated tape laying machines Market is estimated to be valued at US$ 355.11 Mn in 2024 and is expected to exhibit a CAGR of 4.1% over the forecast period 2024 to 2030 Key Takeaways Key players operating in the Automated Fiber Placements And Automated Tape Laying Machines are Callaway Golf Company, Sumitomo Rubber Industries, Nike Inc., Acushnet Holdings, Mizuno Corporation, Taylormade Golf Company Inc., Adidas Group, Bridgestone Corporation, Puma SE, PING, and Anta Sports Products Limited (Amer Sports). The growing demand for lightweight and fuel efficient aircraft from aerospace industry has propelled the demand for carbon fiber composites. As AFP and ATL machines help automate the production of composite parts using tapes and fibers, their adoption has increased among aircraft and space vehicle manufacturers. The advantages of automated fiber placement over hand laying in terms of low labor requirement, high accuracy and speed of production are driving their demand. Technological advancements have made automated fiber placement and tape laying machines smarter, faster and more efficient. Use of robotics, machine learning and data analytics is helping optimize process parameters and composite part design for minimal material usage and maximum strength. Adaptive machines capable of self-correcting during the layup process ensure higher quality outputs. Market trends There is an increasing emphasis on developing modular AFP and ATL machines capable of adapting to different component sizes and shapes through automated adjustment of process parameters. Manufacturers are also focusing on integrating quality inspection systems within these machines to directly monitor fiber/tape placement accuracy, tension and overlap during production. Adoption of collaborative robots has allowed the scaled-down design of AFP and ATL machines. Integrating human-robot collaboration enables production of large as well as complex composite parts with ergonomic advantages. Market Opportunities Growth in demand for carbon fiber composites from automotive industry as OEMs are increasingly adopting them to reduce vehicle weight and improve fuel efficiency presents significant opportunity. The incorporation of carbon fiber in electric vehicles, passenger and commercial vehicles will drive the demand for associated AFP and ATL machines. Focus on developing bi-directional AFP machines capable of achieving ±45° fiber orientations can widen their application in manufacturing more complex net-shaped composite parts. This presents an opportunity for existing players to expand their offerings through R&D. Impact of COVID-19 on Automated Fiber Placements And Automated Tape Laying Machines Market Growth The COVID-19 pandemic has greatly impacted the growth of the Automated Fiber Placements And Automated Tape Laying Machines Market Size . During the peak of the pandemic in 2020-2021, various manufacturing plants had to shut down temporarily due to lockdowns imposed by governments across the globe. This led to a decline in the demand and production of automated fiber placements and automated tape laying machines as the end-use industries such as aerospace and defense, wind energy and others saw a slump in their operations. The supply chains were disrupted significantly which caused issues in the procurement of raw materials for machine manufacturing. International trade restrictions further exacerbated the supply issues. Many planned investments in new machines were also postponed by companies during the crisis period as their focus shifted to maintaining liquidity. The steep fall in demand negatively impacted the market revenues during this time frame. However, with vaccination drives progressing well in most countries and economic activities resuming gradually post lockdowns, the market is witnessing signs of recovery from 2022 onwards. The pent-up demand coupled with delayed projects being implemented is boosting orders for new machines. Government incentives and funding in sectors utilizing these machines will aid future growth. Original equipment manufacturers are also exploring partnerships and modifying their production strategies to build resilience against future disruptions. If the COVID situation remains under control globally, the market is projected to get back on the growth trajectory from 2024 with expanding applications across industries. Geographical Regions with Highest Value Concentration in Automated Fiber Placements And Automated Tape Laying Machines Market Europe accounts for the largest market share in terms of value currently in the automated fiber placements and automated tape laying machines industry. Countries like Germany, France, Italy and UK are prominent aerospace manufacturing hubs with major OEMs and tier players based here contributing to considerable demand. Strong focus on advanced composites by the aerospace sector for lightweighting aircrafts drives machine installation. North America follows Europe with the US spearheading machine usagemajorly in aviation, wind power, transportation and marine applications. Presence of Boeing, Lockheed Martin, GE and others supporting the regional market. Asia Pacific is witnessing fastest growth led by China, Japan, Korea and India. Burgeoning wind energy sector and increasing local aircraft production fostering new investments. Fastest Growing Regional Market for Automated Fiber Placements And Automated Tape Laying Machines Asia Pacific region is poised to be the fastest growing market for automated fiber placements and automated tape laying machines during the forecast period. This is attributed to factors such as rapid infrastructural development, growing emphasis on renewables particularly wind and tidal energy and rising aerospace manufacturing in the region. Countries like China, India are expanding their aviation and wind industries supported by government initiatives. Local aircraft OEMs are ramping up capacities. Favorable policies to boost composite materials adoption will drive machine procurement. Korea, Japan have established automotive and electronics base while ramping aerospace presence. Thus increasing localization of manufacturing will majorly propel the APAC automated fiber placements and automated tape laying machines market. Get more insights on- Automated Fiber Placements And Automated Tape Laying Machines Market Amitriptyline Market Poised To Grow At A Robust Pace Due To Rising Prevalence Of Depression2/29/2024  Amitriptyline Market The amitriptyline market has witnessed significant growth owing to the increasing prevalence of depression globally. Amitriptyline is a tricyclic antidepressant (TCA) that is used primarily for the treatment and management of major depressive disorders. It works by increasing the levels of serotonin and norepinephrine in the brain. The increasing cases of depression and other mood disorders has augmented the demand for amitriptyline as it is one of the most commonly prescribed medications for depression.

The Global amitriptyline market is estimated to be valued at US$ 699.27 Mn in 2024 and is expected to exhibit a CAGR of 5.1% over the forecast period 2024 to 2030. Key Takeaways Key players operating in the amitriptyline market are Adani Wilmar Ltd., Ruchi Soya Industries Ltd, Associated British Foods plc, Archer Daniels Midland Company, Beidahuang Group, Bunge Limited, Borges Mediterranean Group, Cargill Incorporated, Fuji Vegetable Oil, Inc., Adams Group, American Vegetable Oils, Inc., and Olympic Oils Limited. These players are focusing on new product launches and expansion of their manufacturing facilities across various geographies to strengthen their market presence. The growing geriatric population suffering from various mental health issues is presenting significant growth opportunities for players in the amitriptyline market. Furthermore, increasing awareness about depression treatment is encouraging more people to seek professional help. This is anticipated to drive the demand for amitriptyline medications. Key players are also focusing on expanding their presence in developing regions through collaborations with local distributors. The increasing healthcare expenditure and rapid urbanization in Asia Pacific and Latin America provide huge opportunities for global amitriptyline market players to further increase their revenues. Market Drivers Growing Prevalence of Depression Globally The rising incidence of major depressive disorders around the world has significantly boosted the adoption of amitriptyline medications. According to WHO, over 264 million people suffer from depression globally. The increasing awareness about mental health issues and availability of advanced diagnostics is leading to more reported cases. This is the major factor driving the growth of amitriptyline market. Market Restrain Side Effects Associated with Long Term Use The long term use of Amitriptyline Market Size has been associated with several side effects such as dry mouth, dizziness, constipation, difficulty in urination, skin rash, weight gain, sweating and sexual dysfunction. This limits its use for extended periods. The development of alternative drugs with less side effects poses a major challenge for the growth of amitriptyline market players. However, market players are focusing on new drug formulations to reduce side effects. Segment Analysis The amitriptyline market can be segmented based on dosage form as oral solutions, capsules, tablets. Tablets account for the largest share as they are easy to consume and handle. Dry mouth is a common side effect of amitriptyline that make oral solutions less preferred. Generic versions are dominating the tablets segment due to lower costs. The market can also be segmented into hospital pharmacy, retail pharmacy, online pharmacy based on distribution channels. Retail pharmacy has the largest share since amitriptyline is commonly prescribed for neuropathic pain and depression which doesn't require special supervision. It is also easily available over the counter without prescription in most countries contributing to the retail segment. Regional Analysis North America is the fastest growing region in the amitriptyline market and accounts for over 35% share currently led by the US. High awareness about mental health issues and growing acceptance of antidepressants are driving the growth. Europe follows next with over 30% share led by major markets like Germany, UK, France. Asia Pacific is projected to witness highest CAGR during the forecast period with increasing healthcare expenditure and focus on expanding access to mental health treatments in countries like China and India. Latin America and Middle East & Africa also show promising growth potential but have lower overall shares currently due to availability and affordability challenges. Get more insights on- Amitriptyline Market Check more trending articles related to this topic: Organic Farming Market  Aniline Market The global aniline market plays a vital role in the production of various industrial and commercial products. Aniline is an aromatic amine compound primarily used in the production of polyurethane foam, MDI, rubbers, dyes, and agricultural chemicals. It provides properties like flexibility, durability, and resistance to chemicals and abrasion to the final products. Aniline finds widespread usage in insulation, glues & adhesives, electrical switching gear, refrigerator linings, and infant car seats.

The Global Aniline Market is estimated to be valued at US$ 22032.95 Billion in 2024 and is expected to exhibit a CAGR of 10% over the forecast period 2024 to 2030. Key Takeaways Key players operating in the aniline market are Nokia Corporation, Ciena Corporation, Cisco Systems Inc., Huawei Technologies Co. Ltd, ZTE Corporation, Fujitsu Corporation, Infinera Corporation, Telefonaktiebolaget LM Ericsson, NEC Corporation and Yokogawa Electric Corporation. With the growing polymers industry, the demand for aniline is increasing at a rapid pace. The ever-growing construction and automotive industries are also contributing to the rising consumption of aniline globally. Several manufacturers are focusing on expanding their production capacities and global footprint to leverage the vast market opportunities. Key players operating in the Aniline Market Size are Nokia Corporation, Ciena Corporation, Cisco Systems Inc., Huawei Technologies Co. Ltd, ZTE Corporation, Fujitsu Corporation, Infinera Corporation, Telefonaktiebolaget LM Ericsson, NEC Corporation and Yokogawa Electric Corporation. The growth of the polymers industry has augmented the consumption of aniline considerably. Polymers find widespread usage in varied applications such as consumer goods, packaging, automotive, construction and more. This has created robust demand for aniline from the polymers sector. The growing construction and automotive industries have also propelled the global aniline market growth substantially. Developing regions across Asia Pacific and Latin America are witnessing exponential growth of the construction sector which utilizes significant amounts of aniline based products like paints, coatings, adhesive etc. Meanwhile, the flourishing automotive industry employs aniline to produce essential components and interiors of vehicles. Market key trends One of the key trends witnessed in the global aniline market is the shifting production bases. With growing environmental regulations regarding aniline emissions in countries like China and India, major manufacturers are exploring opportunities in other Asian nations and North America with relatively lenient norms. Thailand, Vietnam and Mexico have emerged as attractive investment destinations for setting up aniline production facilities. This allows companies to cater to the rising domestic and international demand, while complying with stringent emission standards in their existing locations. Porter's Analysis Threat of new entrants: High capital requirement in terms of manufacturing facilities and developing infrastructure act as entry barriers for new players in the market. Bargaining power of buyers: Buyers have moderate bargaining power due to availability of substitutes and supply contracts with leading manufacturers. Bargaining power of suppliers: A handful of suppliers dominate the market and supply critical raw materials, giving them significant bargaining power over buyers. Threat of new substitutes: Ongoing R&D in material science to develop new chemical substitutes and green chemicals pose threat of substitution. Competitive rivalry: The aniline market comprises large established market players adopting strategies like new product developments and partnerships to gain competitive advantage. Geographical Regions East Asia accounts for the largest share of the global aniline market in terms of value owing to presence of large consumer bases and manufacturing clusters in countries like China and Japan. South Asia Pacific region is expected to witness fastest growth during the forecast period due to rapidly expanding end-use industries in emerging economies like India, Indonesia and Vietnam driving aniline demand in the region. Get more insights on- Aniline Market Check more trending articles related to this topic: Stem Cells Market  Drug Device Combination Products Market Drug device combination products refer to medical products that combine both drug and medical device components into a single product to provide therapeutic treatment. These products integrate drugs with medical devices such as inhalers, injector pens, transdermal patches etc. for delivery of drugs in the body. Drug device combination products offer advantages such as improved effectiveness, enhanced patient compliance and safety. The growing burden of chronic diseases and rising demand for specialized delivery of drugs is fueling the demand for drug device combination products.

The Global Drug Device Combination Products Market is estimated to be valued at US$ 173.07 Mn in 2024 and is expected to exhibit a CAGR of 3.7% over the forecast period 2024 to 2030. Key Takeaways Key players operating in the Drug Device Combination Products are Evonik Industries AG (RAG-Stiftung), JSR Corporation, Kumho Petrochemical Co. Ltd., Kuraray Co. Ltd., Lanxess AG, Nippon Soda Co. Ltd., Reliance Industries Limited, Saudi Basic Industries Corporation (Aramco Chemicals Company), Synthomer PLC, Synthos (Ftf Galleon S.A.), UBE Corporation, Versalis (Eni S.p.A.). The Global Drug Device Combination Products Market Size is driven by the growing disease burden of chronic diseases such as diabetes, cardiovascular diseases, respiratory diseases etc. Drug device combinations provide targeted, controlled and sustained drug delivery which enhances patient compliance especially for conditions requiring long term treatment such as diabetes, cancer etc. Geographically, North America currently dominates the global drug device combination products market owing to high adoption of technologically advanced medical products and high healthcare expenditure in the region. However, Asia Pacific is expected to witness highest growth during the forecast period owing to rapidly developing healthcare infrastructure, rising healthcare expenditure and expanding patient pool in the region. Market key trends Personalized drug delivery through 3D printing of drug device combinations is a key trend in the market. 3D printing allows development of customized drug delivery devices according to specific patient needs such as dosage, size of dosage etc. This enhances effectiveness and safety of treatment. Furthermore, increasing demand for self-administrable drug delivery devices is another major trend being witnessed in the market. Convenient self-administration improves treatment compliance. Connected drug delivery devices that can track dosage intake and transmit data are gaining increased uptake. Porter's Analysis Threat of new entrants: Low barriers to entry due to availability of resources but established players have strong brand value and distribution network. Bargaining power of buyers: Large pharmaceutical companies have significant bargaining power due to volume purchases but smaller companies have less bargaining power. Bargaining power of suppliers: Few large suppliers and intellectual property rights provides some bargaining power to suppliers but potential for forward integration reduces their power. Threat of new substitutes: Threat of new substitutes is low as devices and drugs work together but new technologies can provide substitute options. Competitive rivalry: Intense competition among major players to gain market share and develop new drug delivery systems. Patent expirations increase competition. Geographical Regions North America region accounts for the largest share in the drug device combination products market in terms of value due to growing prevalence of chronic diseases, increasing demand for healthcare services and presence of major players in the region. Asia Pacific region is expected to witness the fastest growth during the forecast period owing to rising healthcare expenditure, large patient population, increasing awareness about combination products and improving healthcare infrastructure in emerging economies like China and India. The United States accounts for the major share in the drug device combination products market owing to the rising incidence of chronic diseases, growing geriatric population, strong reimbursement policies and technological advancements in the country. China market is expected to grow at a high rate due to rising healthcare expenditure, increasing prevalence of lifestyle diseases, growing demand for healthcare services and large patient population. Get more insights on- Drug Device Combination Products Market Check more trending articles related to this topic: secondary batteries market |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

June 2024

Categories |

RSS Feed

RSS Feed